Social Security Act

Francis Townsend, a doctor, lost his job during the Great Depression and was forced into retirement. William E. Leuchtenburg, the author of Franklin D. Roosevelt and the New Deal (1963), has argued: "He was sixty-seven years old, and had less than a hundred dollars in savings. Disturbed not only by his own plight but by that of others like him - elderly people from Iowa and Kansas who had gone west in the 1920's and now faced the void of unemployment with slim resources." (1)

In 1933 Townsend and Robert Earl Clements, a real estate promoter, proposed a scheme whereby the Federal government would provide every person over 60 a $200 monthly pension (roughly $2,600 in today's money), on condition that he or she retire from all gainful work and spent the money in the United States. Townsend claimed that his Old Age Revolving Pension Plan could be financed by a 2 per cent tax on business transactions. Townsend argued that his plan would help the economy as older people would be compelled to surrender their positions to the younger unemployed and the spending of the pension money would produce a demand for goods and services that would create still more jobs. (2)

Some critics described Townsend's plans as being an example of the ideas of the "crackpot Left". (3) Other observers pointed out that it was far from radical and appealed to Protestant rural America and proclaimed traditional values, and promised to preserve the profit system free from alien collectivism, socialism and communism. In the words of Townsend, the movement embraced people "who believe in the Bible, believe in God, cheer when the flag passes by, the Bible Belt solid Americans." He told his followers: "The movement is yours, my friends... Without you I am powerless but with you I can remake the world for mankind." (4)

Walter Lippmann observed: "If Dr. Townsend's medicine were a good remedy, the more people the country could find to support in idleness the better off it would be." Townsend replied "My plan is too simple to be comprehended by great minds like Mr. Lippmann's." (5) One historian has pointed out that "Townsend meetings featured frequent denunciations of cigarettes, lipstick, necking, and other signs of urban depravity. Townsendites claimed as one of the main virtues of the plan that it would put young people to work and stop them from spending their time in profligate pursuit of sex and liquor." (6)

Franklin D. Roosevelt and Old Age Pensions

Townsend plan would have diverted 40 per cent of the national income to 9 per cent of the people. It obtained a great deal of public support and by 1935 his Townsend Club had over 5 million members. Most of them from among otherwise conservative people, that politicians throughout the country had to take these ideas into consideration. The pressure increased when Townsend handed in to President Franklin D. Roosevelt a petition supporting the Old Age Revolving Pension Plan that had been signed by over 20 million people. (7)

Frances Perkins, one of Roosevelt's most senior colleagues, later recalled in her autobiography, The Roosevelt I Knew (1946): "One hardly realizes nowadays how strong was the sentiment in favour of the Townsend Plan and other exotic schemes for giving the aged a weekly income. In some districts the Townsend Plan was the chief political issue, and men supporting it were elected to Congress. The pressure from its advocates was intense." (8)

The measures taken by President Roosevelt did help 2 million people to find jobs by 1934 but unemployment remained high at 11.3%. The nation's GDP registered a 17% increase on 1933 but national income was still little better than half of what it had been in 1929. Roosevelt and the Democrats were worried about the outcome of the mid-term elections in November, 1934. However, they were wrong to be concerned as the government was rewarded for its actions to deal with the country's economic problems. In the House of Representatives the Democratic majority increased from 310 to 322 and in the Senate they now held 69 seats that was more than a two-thirds majority. Never in the history of the Republican Party had its percentage in either House been so low. Arthur Krock wrote in the The New York Times that the New Deal had won "the most overwhelming victory in the history of American politics". (9)

These results gave President Roosevelt to introduce more radical policies. On 17th January, 1935, Roosevelt asked Congress to pass social security legislation. The two men he chose to guide this measure through Congress had both experienced poverty. Robert Wagner (Senate) was an immigrant boy who had sold newspapers on the street and David John Lewis (House of Representatives) had gone to work at nine in a coal mine. (10)

Roosevelt told the American people: "We must begin now to make provision for the future. That is why our social security program is an important part of the complete picture. It proposes, by means of old age pensions, to help those who have reached the age of retirement to give up their jobs and thus give to the younger generation greater opportunities for work and to give to all a feeling of security as they look toward old age. The unemployment insurance part of the legislation will not only help to guard the individual in future periods of lay-off against dependence upon relief, but it will, by sustaining purchasing power, cushion the shock of economic distress. Another helpful feature of unemployment insurance is the incentive it will give to employers to plan more carefully in order that unemployment may be prevented by the stabilizing of employment itself. (11)

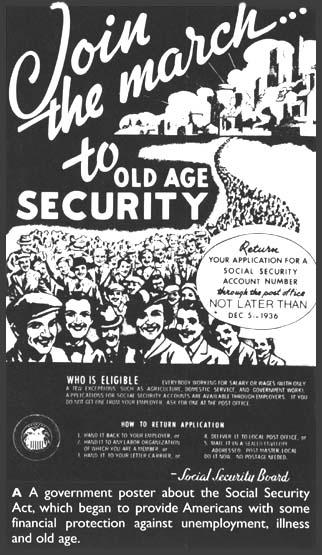

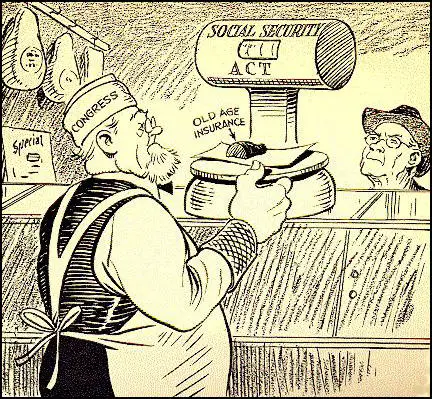

Social Security Act

The Social Security Act established Old Age and Survivors' Insurance that provided for compulsory savings for wage earners so that benefits may be paid to them on retirement at 65. To finance the scheme, both the employer and employee had to pay a 3% payroll tax. The provisions of the act also encouraged states to deal with social problems. It did this by offering substantial financial help the states provide unemployment benefits, old-age pensions, aid to the disabled, maternity care, public health work and vocational rehabilitation. (12)

In the debate in Congress, Arthur Harry Moore protested that if the legislation was passed: "It would take all the romance out of life. We might as well take a child from the nursery, give him a nurse, and protect him from every experience that life affords." Newspapers were also hostile to these measures. For example, The Jackson Daily News reported: "The average Mississippian can't imagine himself chipping in to pay pensions for able-bodied Negroes to sit around in idleness on front galleries, supporting all their kinfolks on pensions, while cotton and corn crops are crying for workers to get them out of the grass." (13)

After being passed by Congress in April and signed into law by President Roosevelt on 14th August, 1935. William E. Leuchtenburg has argued: "In many respects, the law was an astonishingly inept and conservative piece of legislation. In no other welfare system in the world did the state shirk all responsibility for old-age indigency and insist that funds be taken out of the current earnings of workers. By relying on regressive taxation and withdrawing vast sums to build up reserves, the act did untold economic mischief. The law denied coverage to numerous classes of workers, including those who needed security most: notably farm laborers and domestics. Sickness, in normal times the main cause of joblessness, was disregarded. The act not only failed to set up a national system of unemployment compensation but did not even provide adequate national standard." (14)

Despite its faults the Social Security Act of 1935 was a new landmark in American history. It reversed historic assumptions about the nature of social responsibility, and it established the proposition that the individual had the same social rights as those people living in Europe. Roosevelt defended his decision to make the employee contributions so high: "We put those payroll contributions there so as to give the contributors a legal, moral, and political right to collect their pensions and their unemployment benefits. With those taxes in there, no damn politician can ever scrap my social security program." (15)

Roosevelt told Anne O'Hare McCormick: "In five years I think we have caught up twenty years. If liberal government continues over another ten years we ought to be contemporary somewhere in the late Nineteen Forties." (16) The British journalist, Henry N. Brailsford, argued that Roosevelt was doing what David Lloyd George had done between 1906 and 1914, but at a quicker tempo. According to William E. Leuchtenburg: "The British reforms, which rested on the conviction that the profit system was compatible with aid to the underdog, had rendered working-class life less precarious and was one of the important reasons that the depression struck Britain less heavily than America." (17)

This reform came under attack from right-wing conservatives. John T. Flynn argued: "Does anyone imagine that $8 a week is security for anyone, particularly since Roosevelt's inflation has cut the value of that in half? But what of the millions of people who through long years of thrift and saving have been providing their own security? What of the millions who have been scratching for years to pay for their life insurance and annuities, putting money in savings banks, commercial banks, buying government and corporation bonds to protect themselves in their old age? What of the millions of teachers, police, firemen, civil employees of states and cities and the government, of the armed services and the army of men and women entitled to retirement funds from private corporations railroads, industrial and commercial? These thrifty people have seen onehalf of their retirement benefits wiped out by the Roosevelt inflation that has cut the purchasing power of the dollar in two. Roosevelt struck the most terrible blow at the security of the masses of the people while posing as the generous donor of security for all." (18)

Francis Townsend Plan

Francis Townsend claimed that Roosevelt's social security legislation was completely inadequate and in 1936 Francis Townsend joined with Father Edward Coughlin and Gerald L. K. Smith to form the National Union of Social Justice. They selected William Lepke as their presidential candidate. However, Townsend fell out with Smith and denounced him for his fascist sympathies. Coughlin responded by calling the Townsend Plan "economic insanity". Townsend told his followers that if they should vote for either Lepke or Alfred Landon, the Republican candidate. (19)

In the 1936 Presidential Election Townsend gave endorsements to individual candidates and because of his hostility to Roosevelt he refused to give his support to any Democrats. (20) Roosevelt's obtained one of the greatest election victories in American history. Roosevelt won by 27,751,612 votes to 16,681,913 and carried the electoral college 523 to 8. He won every state but Maine and Vermont. Lepke won only 882,479 votes. The Democratic majority rose to 242 in the House of Representatives and 60 in the Senate and Townsend's views on social security were now totally rejected. (21)

After the presidential election support for the Townsend Plan declined rapidly. When he continued to attack Franklin D. Roosevelt and the Democrats. He upset a lot of his followers when he agreed with the Supreme Court wiped out the National Industrial Recovery Act and Agricultural Adjustment Act. On 2nd February, 1937, Roosevelt made a speech attacking the Supreme Court for its actions over New Deal legislation. He pointed out that seven of the nine judges (Charles Hughes, Willis Van Devanter, George Sutherland, Harlan Stone, Owen Roberts, Benjamin Cardozo and Pierce Butler) had been appointed by Republican presidents. Roosevelt had just won re-election by 10,000,000 votes and resented the fact that the justices could veto legislation that clearly had the support of the vast majority of the public. Roosevelt suggested that the age was a major problem as six of the judges were over 70. Roosevelt announced that he was going to ask Congress to pass a bill enabling the president to expand the Supreme Court by adding one new judge, up to a maximum off six, for every current judge over the age of 70. (22)

Townsend was now seen as a opponent of the New Deal. He now lost the support of most of the leading figures in the movement. The vice-president and twelve officials at national headquarters resigned. The editor and most of the staff of the Townsend National Weekly left their jobs in protest against Townsend's comments. Those who left issued a statement claiming that Townsend "was abusing the trust placed in him by the Townsendites, who had signed on to an organisation devoted to the pension-recovery program." In return, Townsend denounced them all as "self-serving traitors." Townsend's organisation continued for several more years but it no longer had any political impact on the American government. (23)

Primary Sources

(1) Jean Edward Smith, FDR (2007)

The most benign, yet in some ways the most serious, threat was headed by Dr. Francis Everett Townsend, an unemployed physician in Long Beach, California. Townsend proposed to pay a monthly pension of $200 (roughly $2,600 currently) to every citizen over sixty, on the condition that he or she retire and promise to spend the sum within the coming month. Pensions would be financed by a business transaction tax of 2 percent. Advocates argued that this would reduce unemployment because older workers would yield their jobs to younger people who had none. And the mandatory spending of pension checks would produce a demand for goods and services that would create still more jobs. The Townsend Plan was far from radical. It appealed to heavily Protestant rural America, proclaimed traditional values, and promised to preserve the profit system free from alien collectivism, socialism, and godless communism.... It was a movement FDR dared not ignore.

(2) William E. Leuchtenburg, Franklin D. Roosevelt and the New Deal (1963)

An unsuccessful country practitioner, Doctor Townsend had migrated to Long Beach, California, in 1919. When various promotional schemes failed, he took a job as a public health official. A change of administration cost Townsend tend his position. He was sixty-seven years old, and had less than a hundred dollars in savings. Disturbed not only by his own plight but by that of others like him-elderly people from Iowa and Kansas who had gone west in the 1920's and now faced the void of unemployment with slim resources - Townsend came up with a plan which he believed would get the country once more on the road to recovery and which would, incidentally, provide security for the aged.

In January, 1934, Townsend and Robert Clements, a real estate promoter, set up Old Age Revolving Pensions, Limited. They proposed to pay a pension of $200 a month to every citizen over sixty (save for habitual criminals), on condition that he or she retire from all gainful work and promise to spend the sum within one month in the United States. The pension would be financed by a 2 per cent tax on business transactions which would be paid into a "revolving fund". The Townsendites argued that their plan would end mass joblessness both because older people would be compelled to surrender their positions to the younger unemployed and because the rapid spending of pension checks would produce a demand for goods and services that would create still more jobs.

Student Activities

Economic Prosperity in the United States: 1919-1929 (Answer Commentary)

Women in the United States in the 1920s (Answer Commentary)

Volstead Act and Prohibition (Answer Commentary)

The Ku Klux Klan (Answer Commentary)

Classroom Activities by Subject